Square_Tea4916

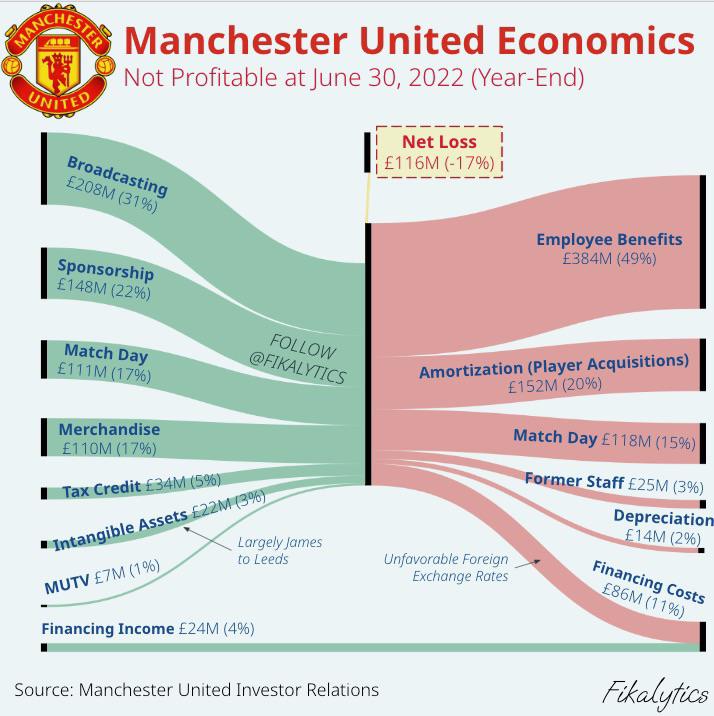

[OC] Manchester United Income and Expenses Breakdown of their 2022 Annual Report

[OC] Manchester United Income and Expenses Breakdown of their 2022 Annual ReportSubmitted by Square_Tea4916 t3_10qi1sg in dataisbeautiful

[OC] Walmart's 2022 Income Statement visualized with a Sankey Diagram

[OC] Walmart's 2022 Income Statement visualized with a Sankey DiagramSubmitted by Square_Tea4916 t3_10il2gw in dataisbeautiful

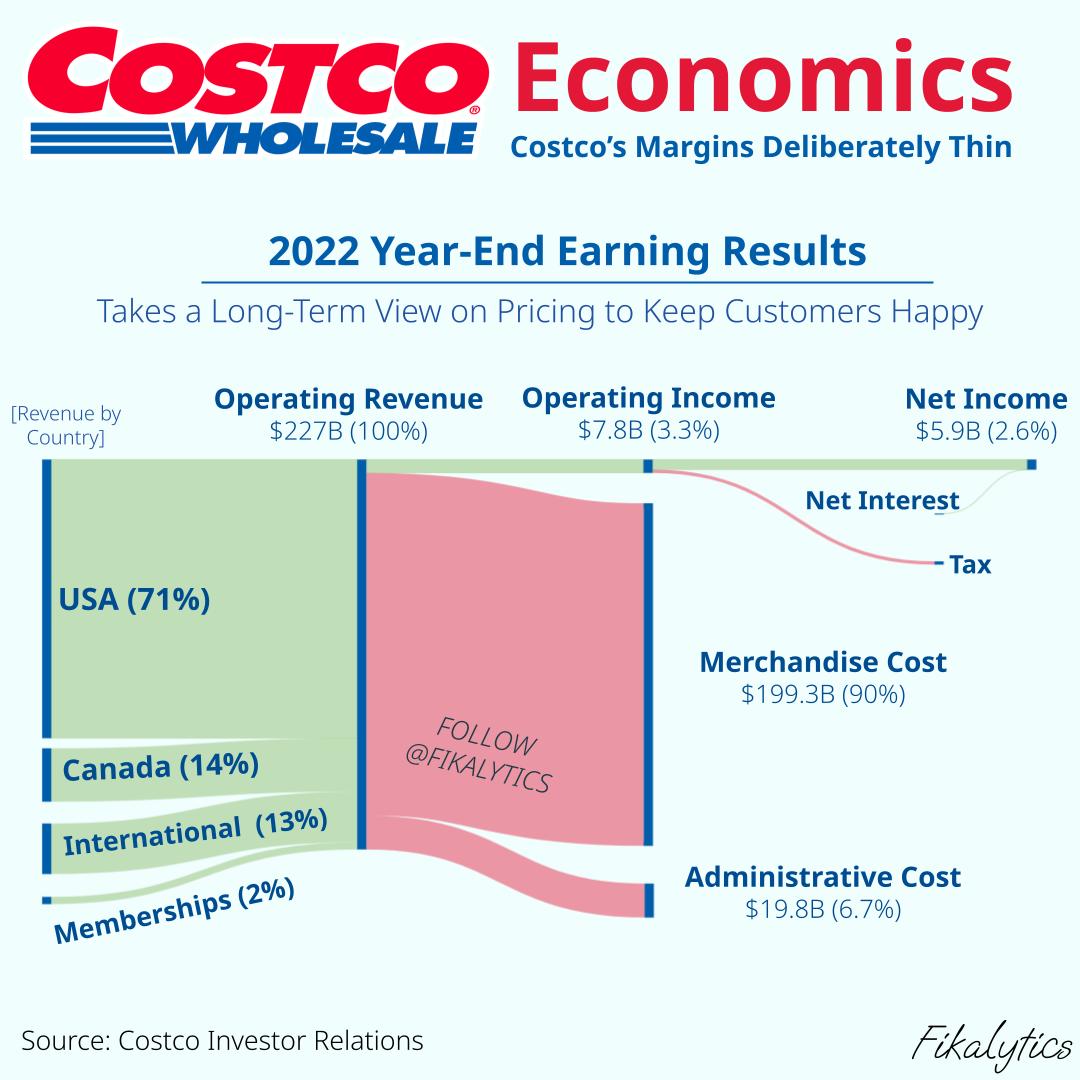

[OC] Costco's 2022 Income Statement visualized with a Sankey Diagram

[OC] Costco's 2022 Income Statement visualized with a Sankey DiagramSubmitted by Square_Tea4916 t3_10hsaf8 in dataisbeautiful

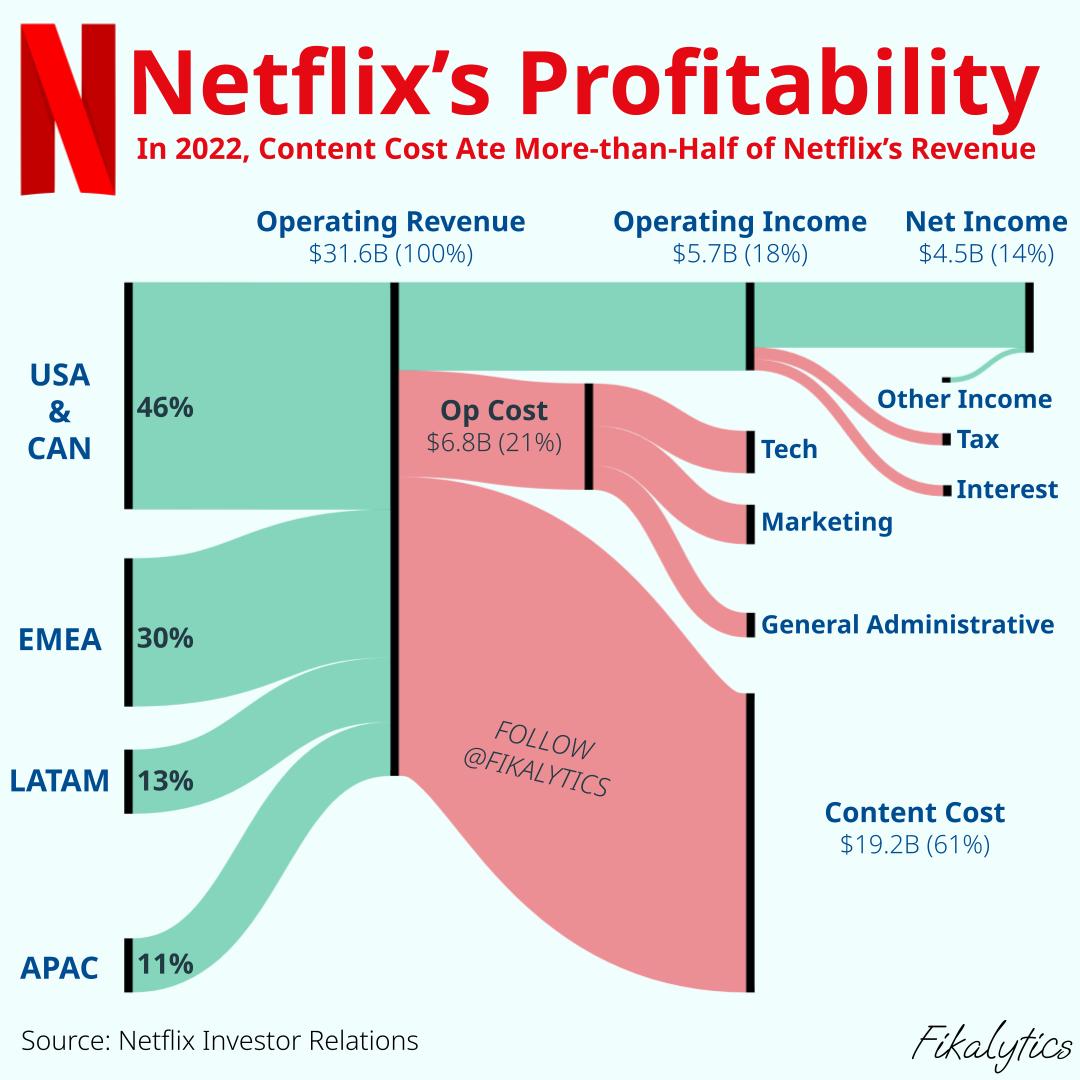

[OC] Netflix's 2022 Income Statement with Sankey (v2 thanks for calling out a mistype)

[OC] Netflix's 2022 Income Statement with Sankey (v2 thanks for calling out a mistype)Submitted by Square_Tea4916 t3_10hi79w in dataisbeautiful

Submitted by Square_Tea4916 t3_10qi1sg in dataisbeautiful

Submitted by Square_Tea4916 t3_10il2gw in dataisbeautiful

Submitted by Square_Tea4916 t3_10hsaf8 in dataisbeautiful

Submitted by Square_Tea4916 t3_10hi79w in dataisbeautiful

Square_Tea4916 OP t1_j6q4usa wrote

Reply to [OC] Manchester United Income and Expenses Breakdown of their 2022 Annual Report by Square_Tea4916

Source: https://ir.manutd.com/financial-information/annual-reports/2022.aspx Tool: SankeyMATIC